With each passing day, the new COVID-19 case count has been

diminishing in Ontario.Today’s tally

was 114 and there were zero deaths.Indeed, the number of daily deaths has been in the single digits since

July 1st.For Thunder Bay District,

the last while has seen a zero daily case count more often than notThere are only two active cases in the

District and the hospital has no COVID cases.And vaccination

rates continue to grow with 69 percent of all people in Ontario having

received at least one dose and 47 percent being fully vaccinated with two

doses.For the time being, the pandemic

is practically over, and the province is slowly reopening its economy with the third stage

set to begin this Friday.

Moving forward, the challenge is many-fold.First, the damage done to the economy is

significant.Ontario had the most protracted lock down in Canada and indeed in much of the developed world. There are many businesses

that after such a protracted lock down will not reopen.The implications for business formation and

investment is serious.Moreover, the

reopening is proceeding at such a slow pace that it may indeed be too late for

many businesses.Employment is

rebounding but we are still not where we were before the pandemic.In 2019, total employment in Ontario stood at

7.377 million employed persons.In 2020

it fell to an annualized 7.022 million. As of June 2021, the most recent numbers

suggest that at 7.273 million, we are still not there yet.

And, try getting anything done.Employment and labour force participation have

both shrunk. The labour shortage which has been underway due to the aging of the population has been made worse with the shutdown and withdrawal of labour not to mention the reduced immigration of the last year. Indeed, if Thunder Bay is

any indicator, trying to get anything done in terms of household repairs and

services is very difficult. Everyone is booked and prices have gone up.Thunder Bay was always a difficult place to

get things done without a bevy of personal connections often acquired in high

school and the problems seem to have become worse in the wake of the

pandemic.

Yet the recovery continues, but much depends on what happens

next with the pandemic.The summer is a

golden time and for the post-pandemic recovery to continue beyond September vaccination rates must continue to rise.With new variants percolating around the world and travel resuming,

getting total double vaccination rates above 80 percent is crucial.September and the return to more indoor activity

will be an important test as to whether or not we really have got things under control.

While it is important to relax restrictions as normalcy

returns there is one restriction that should be maintained for the remainder of

the summer and into the fall and it should be a very simple one – if you are in

an indoor public space, you must wear a mask.It is true other provinces are already moving away from this but in my

opinion this is premature.I think you

can probably open everything up for indoor activity – gyms, theaters, dining etc…

with fairly generous capacity constraints but the one thing that should be maintained

is a face mask particularly this fall. Even in a restaurant, except at your table with your

designated dining partner or party, there needs to be a face mask on the way in

and as soon as you leave your table with servers always masked.It’s a simple rule and one with the greatest

benefits in preventing a resurgence until the vaccination rates are much

higher.

Whether we are up to this final task or plan to throw this

modest caution to the winds remains to be seen.

The IMF has released the October 2020 edition of its fiscal

monitor and economic indicator numbers for world economies and its World

Economic Outlook report titled “A Long and Difficult Ascent” paints a pretty gruesome picture of the

carnage wrought by the COVID-19 pandemic.While the global economic growth outlook has improved somewhat from its

June 2020 report, it is still projected at -4.4 percent and is surrounded by a

fair amount of risk.

However, in the end, performance is relative and what is

more interesting is how different advanced economies are expected to fare in

2020.Moreover, what is also of interest is their

performance economically and fiscally relative to their pandemic performance –

which certainly should be of interest to Canadians.Polling

results have often

indicated that Canadians have largely approved of the way that their

governments have responded to COVID-19 and an international ranking places Canada

near the

top of countries whose public thinks their country has handled COVID-19 well.How justified is this perception by

Canadians?

In understanding how well Canada has done dealing with

COVID-19, one has to start with how Canada ranks in terms of the severity of

the disease which in itself can indicate how good a job Canada has done in

limiting its spread.Figures 1 and 2

plot the ranked total number of COVID-19 cases per 1 million population and the

deaths from COVID-19 per 1 million people as of October 17th (as taken from Worldometer) for 35

advanced economies as defined by the IMF.Cases per 1 million ranged from highs of 32,914 and 25,083 for Israel

and the United States to lows of 490 and 376 for Korea and New Zealand respectively.COVID deaths per million people ranged from

highs of 893 and 722 for Belgium and Spain (with the USA third at 675) to lows

of 5 for both New Zealand and Singapore.

Canada ranks 21st in total cases per million –

putting it in the bottom half of incidence severity – but 10th

highest in deaths per million population putting it in the top third.So, while Canada was not hit as hard by

infections compared to many countries, it was among those seeing higher death rates – largely because of its poor handling of the long-term care sector

where over 80 percent of the deaths occurred.While Canada is not the United States or Spain or Belgium in terms of

the incidence and mortality of COVID-19, it is not Australia or New Zealand or Korea

either. One might argue being an island helps but it did not help Cyprus or Malta that much.

How about the economic impact? Figures 3 to 6 are based on the IMF October

2020 World Economic Outlook Report. Figure

3 ranks the 35 advanced economies in terms of their projected 2020 real GDP

growth rates and here Canada ranks 24 out of 35.While everyone is going to see their economy

shrink, some are going to be hit worse than others. Canada is basically at the

top of the bottom third with an anticipated drop in real GDP for 2020 of -7.1

percent.Overall, it is sandwiched

between highs of -1.8 and -1.9 percent for Lithuania and Korea and lows of

-10.6 and -12.8 for Italy and Spain. Figure 4 ranks these same countries according

to their estimated 2020 unemployment rate and here Canada is an honorary Mediterranean

country where at 9.7 percent it is coming 4th out of 35 countries –

behind Greece, Spain and Italy.And if

one looks at the percentage point increase compared to 2019, Canada’s is a 4

percent point increase.Based on Figure

5, we are the second worse increase of the 35 advanced countries, behind the

Americans who are expected to see a 5.2 percent point rise in their

unemployment rate.

Of course, one might think that Canada’s somewhat mediocre performance

relative to other advanced countries when it comes to the spread of COVID-19 and

its mortality rate may simply be due to the fact that Canada has been a

cheapskate in terms of its public spending compared to other countries.And, by extension, perhaps our economic

performance has been so much worse than other advanced economies because our

federal and provincial governments have been captured by deficit scolds who have foisted restraint upon Canadians.Well, put those notions to rest.When the government deficit to GDP ratios for

these advanced economies are ranked in Figure 6, it appears that Canada is

finally number one in something – the size of its 2020 government deficit

relative to GDP.It is expected in 2020 to

have the largest government deficit to GDP ratio of these 35 advanced economies

registering at 19.7 percent.

Once again, Canada has been spending a lot and seemingly

getting relatively much less for its money.True, we have not done as badly as some countries when it comes to the effects

of COVID-19 on our population (unless you are a resident of a long-term care home) but our economy appears to have been fairly hard hit even with the

many billions of support and assistance that have been funneled into it.Why Canadians have to date been so charitable

towards their federal and provincial governments when it comes to performance

during the COVID-19 pandemic is a bit of a puzzle to me. Perhaps we just like to be nice.

The effects of COVID-19 will transform the international world order and affect Canada’s role in it.

First,

the meteoric rise of China, with its aspirations of world leadership

and greater respect, will come to a crashing halt. Despite the

importance of China’s market to the world economy, there will be an

increase in transactions and transport costs as the hyper-globalized

pre-COVID world takes a pause given concerns about virus transmission.

There

will still be global trade and travel but there will be new rules and

precautions operating as a form of non-tariff barrier with resulting

losses for producers and ultimately consumers. For Canada, trade with

China will continue given the importance of our resource inputs to their

economy. But they will eventually need us more than we need them and

this should shape our trade policy accordingly.

Of course, there’s

also the long-term fallout from the Chinese government’s delay in

alerting the world to the seriousness of COVID-19 while simultaneously

scouring the planet for PPEs. The Chinese government’s desire to be

treated like a superpower runs counter to the leadership and stewardship

we’ve seen over the last few months. With great power comes great

responsibility, and perhaps the best example of it during the 20th

century was the American assistance for European recovery. While

self-interested, the Marshall Plan nevertheless helped former foes and

allies alike rebuild their economies after the Second World War.

Notwithstanding its later efforts, the Chinese government’s behaviour

during the early phases of the pandemic has eroded trust. For Canada,

the new rule in its international dealings with China should be trust

but verify.

Second, the abdication of global leadership and

retreat by the United States is nearly complete, reinforced by its

chaotic handling of its own public health situation. While the U.S. has

been far from perfect, during the 20th century it was a leader for free

markets, international trade and humanitarian efforts to help bring

about a better world. The last four years have seen a populist-fuelled

retreat from this vision of America in the world and we will all be

poorer for it. The COVID debacle in the U.S., due to a lack of

coordination and response, sends a distressing message to its trade

partners and allies. For Canada, there can be no retreat from dealing

with the U.S. given its importance to our economy. But we can no longer

assume that all American interests are automatically our own.

Third,

given what has transpired with both China and the U.S., the Europeans

and the United Kingdom will ultimately assert new leadership, engagement

and involvement in world affairs though they will not always sing with

one voice. The retreat of the U.S., the Chinese government’s lack of

transparency and not-so-subtle bullying—combined with the ever-present

Russian behemoth on their doorstep—means they will need to do more for

themselves in terms of security and trade, and will need to reach out

and strengthen their trade relationships around the world. Here, Canada

has taken the first steps with the Comprehensive Economic and Trade

Agreement but it must actively pursue opportunity and build further

relationships. Trade agreements are not enough, you must work to

implement them.

The ultimate result from all this uncertainty will

likely be an even more competitive and multilateral world order with

Russia, Saudi Arabia, India and Brazil constituting additional elements

of change and disruption. Yet this world will also be a source of

opportunity for a resource rich and diverse outward looking country such

as Canada.

We can benefit, but we must be nimble and adaptable in

this changing world. Canada must actively engage with all players, but

on its own terms, and must seek like-minded allies who are also small

trade-dependent economies with stable, democratic and market-oriented

institutions. Canada, Australia, New Zealand, Taiwan and the

Scandinavian countries can serve as champions of small open economies in

this emerging and more competitive world order. A league of small open

economies may seem naïve, but one should not underestimate the powerful

effects of mice that roar.

This first appeared on the Fraser Institute Blog, May 12 2020.

I have been working on an article surveying the economic history of northern Ontario and thought a summary overview draft of where I am going with it would be a worthwhile post. The entire article is going to be much more detailed but this excerpt below provides a pretty good overview of the direction it is going. Enjoy.

A Very Brief Survey of Northern Ontario Economic History

Livio Di Matteo

Northern Ontario’s

economy began in the 19th century as a booming resource frontier as

a result of favourable international market demand for natural resource commodities which were supplemented by government policy initiatives in transportation and protectionism.

Export-led growth approaches to development suggest that such a growth process

can ultimately expand population and market size leading to self-sustaining

economic growth, but Northern Ontario never made that transition and in the

latter part of the twentieth century and early twenty first century can be

viewed as having undergone arrested development.

Northern Ontario is a vast region of over

800,000 square kilometers covering about 90 percent of Ontario’s land mass.While long the home of a substantial and well

organized indigenous and First Nation population[1],

industrial economic development of northern Ontario under European settlement began in the 19th century as a

booming natural resource frontier driven by rising international market demand

for natural resource commodities – mainly forest and mineral products –

combined with government policy initiatives in transportation infrastructure and economic

protectionism via what was known as the Manufacturing Condition.

In defining the region, it is important to

note that is geographically, geologically and biologically a distinct region

traditionally defined as the area of Ontario north of the French River – Lake

Nipissing – Mattawa River system.It is

essentially Precambrian shield made up of some of the oldest rocks in North

America and as a result of glaciation scraping its soil consists of shallow

soils with some alluvial soil deposits in areas such as the Clay Belt regions

and a mainly boreal forest ecology consisting largely of coniferous forest.[2]

In defining the region there is the

question of borders as some include the Districts of Muskoka and Parry Sound in

northern Ontario – as indeed they are for the purposes of federal and

provincial regional development policies – while other might consider them not

as the north but the ‘near’ north.[3]There is also the question of thinking about

the north as a region given that it is a very diverse area that in many

respects is not one north but ‘many’ norths.[4]

Geographically, there is the Northwest

consisting of the Districts of Thunder Bay, Rainy River and Kenora while the

other two-thirds of the region is the Northeast consisting of Cochrane,

Timiskaming, Algoma, Sudbury, Nipissing and Manitoulin.There is also the vast sparely populated area

north of 50 which in some respects does not fit into either the northeast or

northwest except by government fiat.And

of course, there is a rural remote north of small towns and Indigenous reserves

as well as an urban north consisting of the five major cities – Thunder Bay, Sault

Ste. Marie, Timmins, Sudbury and North Bay.And the Northeast is also marked by a strong francophone population

component while the region as a whole has a large Indigenous population.

The themes of Northern Ontario’s economic

development are three-fold: natural resources, transportation and government.[5]Northern Ontario’s economic development can

easily be discussed within the framework of economic staples – products with a

high natural resource content – given the importance of fur, lumber, pulp and

paper and mineral products to the north’s economic history. As for

transportation, this is a key theme given the importance of the Canadian

Pacific (CPR) and Temiskaming and Northern Ontario Railway (TN & O) in

providing access to northern Ontario resources in the 19th and early

20th centuries as well as providing the means for them to exit the

region to world markets.Finally,

government is important given the federal role in providing transportation

infrastructure that accessed and served the North such as the CPR, the

Trans-Canada Highway and the St. Lawrence Seaway as well as the Ontario

government given its parallel regional development program in the 19th

century consisting of the building of the TN & O as well as the

protectionist Manufacturing condition and its own agricultural land settlement

policy.

Given the importance of natural resources

to northern Ontario’s economy, the analytical framework best-suited to

outlining the causal relationships of the development process is the Staples

Approach or more generally, models of export led development.The Staples approach sees a region’s natural

resource base as the most important determinant of both the pace as well as the

patterns of economic growth with the classic exposition provided by Harold

Adams Innis who viewed economic development as springing from the interplay

between an industrial heartland and a resource reducing hinterland.[6]In the case of northern Ontario, it can be

viewed as a resource hinterland not only to the industrial south but also the

rest of the world economy given the international market for its mineral and

forest products.More modern versions of

the Staples Approach see economic development as the process of diversification

around an export base with the degree of diversification a function of what are

termed economic linkages.These linkages

involve producing inputs for the resource export sector or investing in

industries that use the output of the export sector as an input as well as the

final demand for domestically produced consumer products.[7]

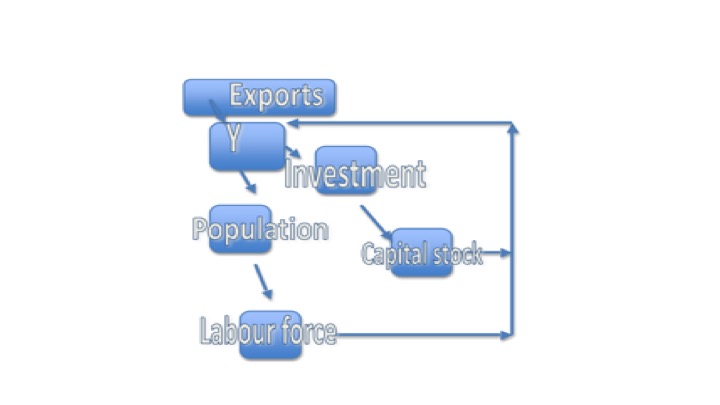

Figure 1 outlines the export led/Staples

growth process with an increase in exports generating an increase in the

regional economy’s output/income (Y).The presence of rising income and economic opportunity in the resource

sector leads to population increase both via natural increase but also

migration into the region.This leads to

an increase in the labour force which feeds back into the generation of

income.As well, the increase in income

leads to an increase in regional saving which fuels investment as well as

external investment flowing into the region to provide the capital stock needed

to expand production of the resource export.This process continues in a circular fashion until both the income and

population become large enough to provide a market for regionally produced goods

and services on top of the export sector and it is this expansion of regional

manufacturing production as well as services to meet local needs and substitute

for imports that becomes the process of diversification.A failure to grow and develop beyond the

initial export industries that powered development can be seen as incomplete or

arrested development.[8]

Figure

1: A Model of Export-Led Growth

The economic history of northern Ontario can be divided into a number of stages. They are: 1) Pre-European Settlement to 1867, 2) Boom, Colonialism and European Settlement, 1867 to 1913, 3) Consolidation, Depression and War, 1914 to 1945, 5) Post-War boom, 1946 to 1969 and 6) Arrested Development: Economic Dependency and Decline, 1970 to the Present.

The economic development of northern

Ontario followed a process of export-led growth fueled in particular by the

export of mineral and forest products.International demand and private sector exploitation of the region’s

resource abundance starting in the 19th century was also accompanied

by investment in transportation networks to bring resources out to market and

government policies and initiatives designed to help facilitate development as

well as take advantage of the public sector revenue potential of these

resources.Within this framework then,

the three major engines of northern Ontario economic development are natural

resources, transportation and government.

During each of northern Ontario’s

development periods outlined here, economic growth was most robust during eras

where all three engines came together to provide the impetus for economic

growth and employment creation.The most

robust economic growth and development occurred during the eras from 1867 to

1913 and 1946 to 1969. Both of these

eras coincided with good global economic conditions which fostered a demand for

resource products and led to private capital investment in production

facilities and transportation networks.Both of these eras also saw a large spending and policy role for

government which facilitated development. The first era also saw northern Ontario as a major source of provincial government revenue.

Growth was poorer in the 1914 to 1945 as a

result of erratic global markets, private sector weakness and the retreat of

government involvement in northern development after the onset of the Great Depression

and yet this was still an era of substantial population growth.Economic growth since 1970 in the region has

essentially stagnated along with population growth as a result of long-term

technological change which reduced the labour intensity of natural resource

extraction in the region.While

government did undertake more interventionist activity in an effort to arrest

northern decline, it has failed to reverse the slow growth nature of the region

given the absence of supporting private sector investment.

[1]By the 17th

century, the mainly Algonkian culture Anishnawbe and Cree indigenous population

had developed a seasonal woodland economy and lifestyle centered on hunting and

trading. See Bray and Epp (1984: 8).

[2] See Robinson (2016: 8-9) for a fuller description of the

region.The glaciers of the various ice

ages periodically scraped topsoil off in northern Ontario and deposited it

further south ironically enough making nature responsible for the first set of

“resource transfers” from Ontario’s north to the south. According to Louis

Gentilcore (1972: 7-8): “The acid nature of the podzols, the slower breakdown

of the vegetable matter, and the prevalence of peaty soils create problems in

the utilization of the soils of northern Ontario for commercial agriculture.”

[3]The 2011 provincial

Growth Plan for Northern Ontario (2011) for example includes Parry Sound.

[7]These are generally

known as backward, forward and final demand linkages.See Watkins (1963).

[8]Part of this process

of arrested development could also be referred to as a Staples Trap whereby an

economy is not able to move beyond its initial export sector activities.For a discussion of the Staples Trap see

Watkins (1963).

References

Bray, M. and E. Epp, eds. (1984) A Vast and

Magnificent Land: An Illustrated History of Northern Ontario. Ontario Ministry

of Northern Affairs.

Di Matteo, L. (1991) “The Economic

Development of the Lakehead During the Wheat Boom Era: 1900-1914,” Ontario

History, LXXXIII, 4, December, 297-316.

Di Matteo, L. (1999) “Fiscal Imbalance and

Economic Development in Canadian History: Evidence from the Economic History of

Ontario,” American Review of Canadian Studies, Summer, 287-327.

Innis, H.A. (1930/1984) The Fur Trade in

Canada, Toronto: University of Toronto Press.

Miller, T. B. (1985) “Cabin Fever: The

Province of Ontario and its Norths.” In D.C.D.C. MacDonald, ed., The Government and Politics

of Ontario. 3rd ed. Scarborough:Nelson, Canada, 174-191.

Ontario (2011) Places to Grow: Growth Plan

for Northern Ontario.Toronto: Ministry

of Infrastructure and Ministry of Northern Development, Mines and Forestry.

Robinson, D. (2016) Revolution or

Devolution?: How Northern Ontario Should Be Governed. Northern Policy

Institute. Research Paper No. 9, April.

Watkins, M. (1963) “A Staple Theory of

Economic Growth,” Canadian Journal of Economics and Political Science, 29,

141-158.

The most recent

set of crime statistics for Canada revealed that police-reported crime in

Canada, as measured by both the crime rate and the Crime Severity Index (CSI),

increased for the fourth consecutive year in 2018, rising 2%.The accompanying figure below further

reinforces the fact that after years of decline – a decline that stretches back

to the 1990s – crime rates are rising.Of course, all of this begs the question as to why crime rates are

rising again after years of decline.

Explaining the drop in crime rates has been

a

source of some debate.The fall in

crime rates since the 1990s in Canada as well as the United States has been

attributed to a number of factors including new policing strategies, changes in

the market for illegal drugs, an aging population, a stronger economy, tougher

gun control laws and increases in police numbers. As for the impact of the

economy on crime, well that is also a source of debate.

On the one hand, the intuitive feeling is

that a weak economy should cause people to turn to crime.Yet, many studies of the relationship between

the economy and crime have found statistically small relationships between

unemployment and property crime and often no relationship between violent crime

and unemployment.It has also been argued

that economic downturns may actually reduce criminal opportunities as when unemployment

is high more people are at home "protecting" their property and

when out and about they carry less cash and possessions.

If the latter is the case, one could make

the argument that the strengthening economy of the last couple of years has

been a key factor in fueling the recent surge in crime.Unemployment rates in Canada are at historic

lows and to add fuel to the fire – so are interest rates.Low interest rates mean that even if more

employment today is part-time or uncertain, people are still able to consume more and

go out more simply by borrowing more. Indeed,

Statistics Canada also noted recently

that the seasonally adjusted household credit market debt to disposable income

ratio increased to 178.5 percent in the 4th quarter of 2018.

More debt to fuel spending on homes and

basic consumption frees up resources to spend on more illicit things like

illegal drugs and much of the recent crime increase is drug related.

With unemployment low and cheap money

sloshing around both fueling spending and consumption, the opportunities for

crime may have mounted. It is certainly a point worth considering.

Well, in the wake of the release of the 2019 Budget, Prime Minister Trudeau is off to Thunder Bay where he will be hosting a Town Hall on the campus grounds of Lakehead University on Friday March 22nd. Indeed, the preparations for his arrival are already underway as the grounds of the C.J. Saunders Fieldhouse where the event will occur are being swept and tidied up from the accumulated grit of a harsh winter. This is apparently Trudeau’s first visit to Thunder Bay since 2016 which is a signal that the election campaign is already underway. The festivities get underway at 7 pm (but if you want a front row seat you need to register and arrive by 5:00 pm).

Thunder Bay can be considered a relatively politically safe place for the federal Liberals to have a Town Hall given the two ridings have returned mainly Liberals to Ottawa for nearly 100 years. Thunder Bay voters are actually very conservative voters in the sense that they dislike change and always do the same thing – that is, return Liberals to Ottawa. The only way they deviate from their inherent conservatism is to actually vote Conservative. Indeed, the last federal Conservative party politician who was elected was Robert Manion, who if memory serves me correctly, was around in the 1930s. Of course, there was MP Joe Commuzzi circa 2007 – who started as a Liberal but then switched to the Conservatives and served as a Minister– but he was not elected as a Conservative so my initial point stands.

So what issues will Prime Minister Trudeau have to face in Thunder Bay? Well, the audience is likely to be filled with gushing supporters who will hang on his every word and engage in numerous standing ovations despite the recent disillusionment over the SNC-Lavalin-Raybould Affair. Indeed, the Prime Minister is probably looking forward to an evening’s relief from the stress and acrimony of Ottawa. There is nonetheless the potential for some fireworks and charged questions on a number of topics should the Town Hall decide to deviate from what is likely to be a large pep rally. For those who might be interested, here are the parameters of just two interesting question areas.

What is the Federal Government going to do to help Thunder Bay address the December 2018 report by the Office of the Independent Police Review Director on relations between Indigenous People and the Thunder Bay Police Service? It is true that the local police are a municipal function and municipalities are creatures of the provinces, but it remains that First Nations and Indigenous peoples are a very important responsibility for the Federal government. The recommendations for the Thunder Bay Police Service are going to involve a substantial increase in expenditures on an already stretched municipal tax base. Is there any real federal financial assistance coming or is Thunder Bay on its own in dealing with this? Indeed, given that Thunder Bay is a regional centre for health and education services for area First Nations, what can the federal government do to assist in this regard?

As well, what is the Federal Government doing to actually implement its own growth plan for the Northern Ontario economy? All of us are familiar with the 2011 Northern Growth Plan released by the Ontario Liberal government which, over the course of the next 25 years, was supposed to assist the North in reversing its economic decline. Well after five years of the provincial Northern Growth Plan – the plan to end all plans – the population of the North remains flat, employment is down and the value of new investment is also down.

This lacklustre result has not deterred the Federal government from announcing its own Prosperity and Growth Strategy for Northern Ontario in April 2018 with twelve areas of action. However, since then there really has not been much to be seen and heard as to specifics of what this strategy entails, aside from mentioning the strategy whenever there is an announcement of federal money from FEDNOR as was the case in Sudbury in December 2018. Aside from this, there is little to be found in a Google News search when the term "Prosperity and Growth Strategy for Northern Ontario" is typed in. So, is there an actual Federal action strategy for Northern Ontario or is it just another election marketing ploy?

I guess we will have to wait until tomorrow night to see if we learn anything new. I for one expect there will indeed be some entertainment involved in this Town Hall Meeting. Who knows, maybe we'll even get yet another announcement of federal support and commitment for the Ring of Fire? At the very least, in an election year one might expect some federal infrastructure dollars to finish four-laning the highway to Nipigon.

In light of my recent

contributions on China’s economic performance which have appeared in The

Hill and on the Fraser

Institute Blog, I thought it might be useful to provide the figures which

underpin the longer-term analysis of their performance.The data I used is from the Angus

Maddison Database – the 2018 update – and the data is summarized in the

accompanying Figures 1 and 2.

Figure 1 plots total

real GDP from 1820 to 2016 in 2011 USD for the United States, the United Kingdom

and China.In 1820, China had a vastly

larger economy than either the US or the UK with a real GDP of $325 billion compared

to $69 billion for the UK or $21 billion for the USA.Indeed, for much of economic history, China

has always been the biggest economy in the world as a result of its massive

population.In 1820, China had a

population of 381 million people compared to 10 million for the United States

and 21 million for the UK.However, the

19th century was not kind to China and by 1870, China’s economy had

shrunk to $270 billion but it was still larger than the United States at $150

billion and the UK at $179 billion.

Total GDP of both the

US and the UK grew quickly as a result of late nineteenth century

industrialization with the US matching the UK in 1878 and then pulling ahead in

terms of total GDP.By 1887, the US economy

at $306 billion was larger than China at $274 billion and the UK at $228

billion.By the eve of the First World War

in 1913, the US economy at $791 billion was nearly twice the size of both the

UK and China at $368 billion and $344 billion respectively. In the period since

WWI, the United States grew rapidly and by the mid 1970s was over five times

the size of the UK economy and about five times larger than China’s economy.

China had a Communist

revolution in 1949 but economic performance in its aftermath - while substantial - was not as

robust when compared to the last forty years.From 1950 to 1975, China real GDP grows from $348 billion to $1.2

trillion – a tripling of output.However,

things for China really take off with the first economic reforms and liberalization

of the 1970s and from 1975 to 2016, its economy expands from $1.2 trillion to

$17.3 trillion.Over the 1975 to 2016

period, the US economy expanded from $5.6 trillion to 17.2 trillion while the

UK expanded from $1 trillion to $2.5 trillion.

In 2016, China

re-assumed its historical role as the world’s largest economy.Yet, as I pointed out in my oped pieces, this

is not the end of the story.Despite its

impressive and rapid economic growth in terms of total output, China still lags

when it comes to per capita output. As Figure 2 shows, over the entire 1820 to

2016 period, China has always had a lower per capita GDP than either the UK or

the US and the relative gap has not changed all that much despite the rapid

growth of the last 40 years.In 1820, per

capita GDP in China was about 26 percent that of the UK and 41 percent that of

the USA.By 1975, its per capita GDP was

7 percent that of the UK and 5 percent that of the United States.After the robust growth of the post 1975

period, by 2016 per capita Chinese GDP now stands at 34 percent that of the UK

and 24 percent that of the US.

So, China has done

very well but it still has a long way to go.Its rapid extensive growth masks the fact that large swaths of its

population are still quite poor.Its

economy is showing signs of economic

and political fragility given its aging population, large debt levels and

economic inequality and this has global

implications.Such fragility is probably

a reason for its more authoritarian turn in recent years under President Xi Jinping.After the rapid growth and improvement in

living standards of the last few decades, any economic slowdown may create a

politically volatile domestic mix of discontent.