With the Bank of Canada’s recent rate hike and the expectation that there may be another hike in July, the talk of an economic slowdown and a recession has ramped up. There is talk and rumor of looming recession and that has been underway for some time. At the same time, another view is that we risk moving into a 1970s style economic environment if inflation is not soon brought to heel. Given the lag between tighter monetary policy and the economic slowdown that would bring inflation down, it is possible that any downturn is still up ahead. At the same time, the evidence to date suggests the economy is not yet slowing down. Despite higher interest rates, demand is still being fueled by pent up consumer revenge spending, robust population growth – more people means more consumption spending - and residual post-pandemic savings.

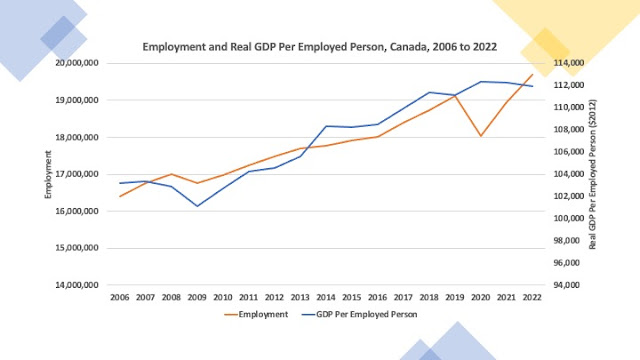

Figures 1 to 3 show that key economic indicators after post-pandemic re-bound and adjustment remain robust. Figure 1 presents the Canadian City CPI total inflation rate (from FRED) and while it has been coming down it is still over five percent and high by the standards of recent history. Figure 2 shows quarterly real GDP growth and while recent growth at about 2 percent is down substantially from the pandemic rebound, it is akin to pre-pandemic growth. There have been no two consecutive quarters of negative real GDP growth – a traditional hallmark of a recession. And while 2 percent growth is not great, that is more a long-term productivity growth problem than anything to do with rising interest rates and recessions. And then there is Figure 3 which shows we are currently at the lowest unemployment rate in over a decade – again more a sign of an overheating economy rather than a harbinger of recession.

So, it would appear that until there is evidence to the contrary, at least another interest rate increase by the Bank of Canada is in the offing. The economy is still growing, labor markets are tight, and inflation remains high by historical standards. The current level of interest rates seems to be compatible with ongoing inflation in the 4 to 5 percent range and is unlikely to bring us to the target 1 to 3 percent range of days of yore. Keeping inflation at the 4 to 5 percent range is dangerous given that any demand or supply side shock when inflation is already in the 4 to 5 percent range could bring us to double digit inflation – a 1970s style scenario.