The Northwestern Ontario Municipal Association (NOMA) will be meeting April 22nd to 24th for its 2026 conference and annual general meeting in Thunder Bay, under the theme “Resilience.” After the winter we have had, resilience is an apt theme though one suspects the choice of theme pertains to the economy and municipal finances rather than the weather and the gauntlet that has become the region’s highways. Economic resilience is especially important these days and it is important to note that the economy in Northwestern Ontario has been doing rather well over the last few years if one is to take labour force data at face value.

It has been an era not of decline or stagnation but of growth with that growth occurring both in the region’s dominant metropolis of Thunder Bay but also outside of it. Indeed, there has been a noticeable improvement in one of the key indicators at least from the general public’s perspective – the unemployment rate. From highs of 8 percent in the wake of the Great Recession and Forest Sector Crisis, the unemployment rate in Northwestern Ontario in 2025 stood at 4.6 percent compared to over 6 percent for Canada and over 7 percent for Ontario. Using data from Statistics Canada, a more detailed portrait of improvement emerges.

Figure 1 plots three labour market indicators for Northwestern Ontario comparing 2015 with 2025. Between these two years, the population aged 15 years and over grew from 173,400 to 184,200. The labour force grew from 104,700 to 112,500 and employment grew from 98,400 to 107,300. Of course, it is worth looking at the data in terms of the Thunder Bay CMA and the rest of the region given that Thunder Bay CMA accounts for about 60 percent of both the population and employment of the entire region.

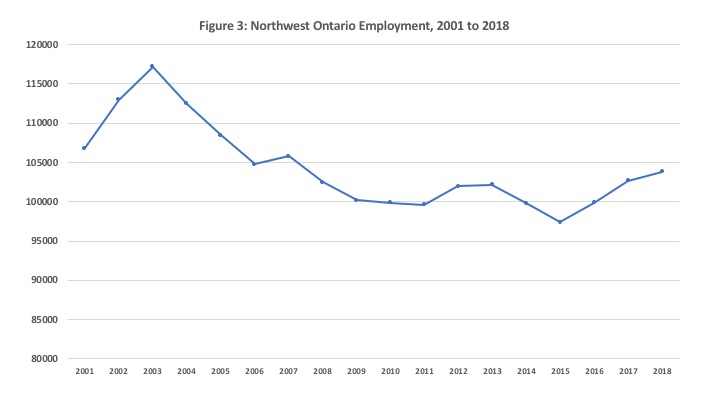

Figure 2 repeats the indicators for the Thunder Bay and adds Full Time(FT) and Part Time (PT) Employment. Thunder Bay’s population aged 15 years and over increased by 7,400 between 2015 and 2025. This was accompanied by labour force growth also of 7,400 individuals and employment growth again of 7,400 with FT employment growing by 8,100 while PT Employment declined by 700 jobs. The good news here is that this employment creation was overwhelming FT employment, and this pattern repeats itself outside of Thunder Bay. Figure 3 shows that for the rest of Northwest Ontario outside of Thunder Bay, the population aged 15 years and over grew by 3,400 with the labour force growing by 400 and employment growing by 1500. FT employment in the region outside Thunder Bay grew by 1,800 while PT employment also declined by 300 jobs.

Figure 4 compares percent growth in these indicators across Thunder Bay and the Rest of Northwest Ontario. Between 2015 and 2025, population aged 15 and over grew 7 percent in Thunder Bay and 5 percent in the rest of the region. The labour force grew nearly 12 percent in Thunder Bay but only 1 percent in the rest of the region. Meanwhile, employment grew 12.5 percent in Thunder Bay and 3.8 percent in the rest of the region. Full time employment grew impressively by nearly 18 percent in Thunder Bay and almost 6 percent outside of Thunder Bay. Part time employment declined more in Thunder Bay at -5 percent as opposed to about -4 percent outside of Thunder Bay.

Figure 5 illustrates the annual unemployment rates in Thunder Bay and the outside region. Both have declined over time with the decline somewhat sharper in the region outside of Thunder Bay. That is because the labour force has expanded more rapidly in Thunder Bay relative to the rest of the region as Thunder Bay has attracted more population growth. Nonetheless, a rising tide appears to have lifted all boats and the improvement in full time employment is especially welcome.

What has been driving these improvements? The construction work both in Thunder Bay and the region whether on the electricity grid or highway improvement has been a factor. Thunder Bay can add housing and hotel construction to this set of projects not to mention a billion-dollar correctional facility. Then there is mining development which continues to generate employment and activity. Of course, the region also benefits from a large public sector and quasi-public sector particularly in the health, social assistance and indigenous economic sectors which has also been a factor in employment growth nationwide. All these sectors in Northwest Ontario have been relatively well sheltered from the ongoing tariff dispute with the United States. While the Northwest has not escaped unscathed from recent employment losses, it remains that much of the fallout has hit the manufacturing sector in southern Ontario.

So, regional municipal delegates and leaders will have a lot to celebrate at this year’s NOMA Meetings. Indeed, this growth should also be reflected in growing municipal tax bases which will afford additional revenue. Yet, it is not time to rest on laurels given that the economy both nationally and globally remains turbulent and uncertain. Hopefully the region will be able to capitalize both on critical minerals mining as well as the growth in defense related spending.